The importance of East Asian markets including China’s in the global financial system and their essential qualities are little appreciated or understood, given the prevailing analytical narrative of global liberalization. In a recently published paper, Johannes Petry of Goethe University Frankfurt and the University of Warwick and Fabian Pape of the London School of Economics and Political Science argue that Asian financial players and their still developmental characteristics have to be considered to understand fully fundamental shifts in the global financial system.

Currency trading in Seoul: The importance of both public and private East Asian capital within the global financial system is underappreciated (Credit: Seoul etc)

After the collapse of Lehman Brothers on September 15, 2008, the bankrupt global powerhouse was broken up and its remaining operations sold to other financial houses that had better withstood the global financial storm. Fending off competing offers from Barclays and Standard Chartered, Japan’s biggest investment bank Nomura acquired Lehman’s Asia-Pacific and European operations, solidifying its foothold in European markets only a year after expanding its US presence through the acquisition of Instinet.

Nomura acquired Lehman’s operations only weeks after state-owned Korea Development Bank had walked away from acquisition talks that could have rescued the American institution, while in March 2008 China’s largest investment bank, CITIC, had launched an (ultimately unsuccessful) bid to acquire the failing US investment bank Bear Stearns.

These early advances of Asian financial players on the global scene foreshadow a larger shift which has – despite its far-reaching implications for the post-crisis politics of global finance – only received limited attention in existing academic and policy debates: the growing importance of both public and private East Asian capital within the global financial system which we explore in a research article that was on March 15 published in the Review of International Political Economy.

Since the 2007-09 global financial crisis (GFC), scholars have located the key dynamics of financial globalization in two distinct areas. The first focuses on money flows associated with macroeconomic imbalances such as the relationship between excess savings and foreign-exchange reserve accumulation in Asian economies on the one hand and the ballooning US debt and deficit on the other hand. This dynamic is sustained by the dominance of the US dollar, which bestows a well-known “exorbitant privilege” on the US to pursue domestic policy without facing external constraints.

In contrast, peripheral states are limited in their ability to use their currency in international trade and finance. In this interpretation, the relative role of major currencies has implications for the balance of power between states, drawing analytical attention to the relationship between major powers in today’s globalized world. Thus, the primary focus of analysis is China’s rise and potential contestation of US (dollar) hegemony. As a result of this binary view, the broader significance of the East Asian region for global finance is often missed.

The second approach abandons the big, geopolitical picture in favor of a more intimate understanding of the role of private finance in the international system: that is, how banks and non-bank actors such as asset managers operate internationally, and how state actors and market instruments become ever-more entangled within the pursuit of stable governance of globalizing private finance. Yet, influenced by the experience of the GFC, these interpretations tend to emphasize the centrality of transatlantic financial relations between the United States and Europe.

In somewhat stylized terms, then, we are presented with a picture in which scholars have focused either on public money flows between the US and China, or on private banking flows between the US and Europe. We argue that this implicit division of labor creates a false dichotomy that ignores the growing importance of private international finance in East Asian economies and their integration into the global financial system.

This generates important shortcomings: by considering the globalization of private finance first and foremost as an Anglo-American or European affair, the governing logics and dynamics of private international finance (both pre- and post-crisis) are tacitly assumed to be informed by transatlantic financial relations. As a result, scholars have largely failed to question whether there is anything distinctive about the interaction of private international finance and East Asian economies, and how such interactions could impact the norms, rules and procedures that govern the global financial system.

Despite offering unique insights into the mechanics of the global financial system, the macro-financial research program suffers from a blind spot regarding East Asia’s rising importance in global finance. In recent years, Asian investors have greatly expanded their operations into global markets and increasingly drive global investment flows. At the same time, East Asian capital markets have grown at extraordinary rates, outsizing and outperforming their European peers as they attract ever more global capital inflows.

Yet, the growing integration of East Asia into global finance should not be likened to a seamless continuation of neoliberal financial deregulation. The integration of East Asian capital signifies not just a quantitative shift within the global system, giving greater weight to the region, but should be seen as an invitation to assess what is qualitatively different about the investment strategies of actors from across the region. What is important is that, instead of converging towards a neoliberal logic that conflates “efficient” outcomes with maximizing (private) profit, the institutional arrangements that underpin financial transactions and relationships in East Asia retain what we refer to as “developmental characteristics”.

Here, finance takes on an important role in facilitating national developmental objectives, thereby blurring the state-market boundary. Where Western states primarily seek to protect the profit-opportunities of their investor base, East Asian developmentalism retains a more strategic and selective approach. East Asia’s rise within global finance thus calls for a reconsideration of conventional analyses which often assume the global financial system’s role as a force of neoliberal globalization that reinforces the (infra)structural power of finance.

To make sense of the changing institutional arrangements that underpin private international finance, we argue that rather than treating global finance with a “one-size-fits-all” frame, the macro-financial framework would benefit from integrating the socially and institutionally grounded differences of various national financial systems into its analysis. By combining the systemic macro-financial view with a comparative perspective, we can develop a novel approach to exploring the geographic shift of international finance towards East Asia.

We analyze the global financial system as constituted by financial flows that are facilitated by globally active financial actors and take place between financial markets which are part of distinct national models of capitalism. By breaking down the global financial system into these observable, constitutive parts, our framework takes into account the role of institutional specifics within the global system.

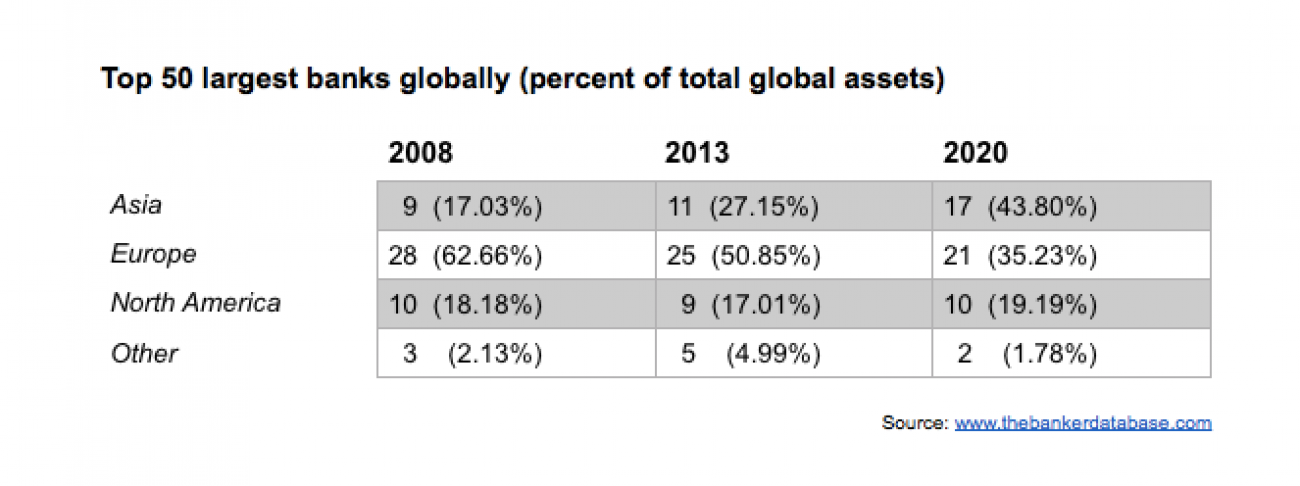

Whereas Europe was crucial to understanding the pre-crisis politics of global finance, today Japanese banks, Korean pension funds, Taiwan life insurers, Hong Kong financial infrastructure and Chinese investment funds are gradually replacing European financial flows, actors and markets as central nodes in the global financial system. Be it the increasing importance of Asian banks, the rise of Asian financial centers, or how Asian markets have both surpassed in size and outperformed their Western peers, we can see the growing importance of East Asia for global financial flows, actors and markets (and the subsequent declining centrality of European finance).

But how do the institutional characteristics that drive the global integration of East Asian financial systems differ (in part) from transatlantic finance?

Focusing on China, Japan, Korea and Taiwan, we analyze Asia’s integration into global finance (global investors in Asian markets) and the internationalization of Asian finance (Asian investors in global markets), as well as the broader implications of this process for the dynamics and politics of the global financial system.

On the one hand, global investors tend to accept the developmental rules of East Asian markets when reallocating investments. While European finance converged towards neoliberalism since the 1980s, developmental characteristics – ideas about the necessity and desirability of strategically governing the economy for nation development purposes – have persisted in East Asian markets, despite an increasing influx of global capital. Whereas China clearly exhibits the most restrictive approach to foreign investors, Korean and Taiwan authorities also actively manage inbound financial flows and foreign investor activities. Even in Japan, which has for a long time been firmly integrated into global financial circuits, neoliberal logics have not fully replaced existing institutional configurations.

While the aggregate volume of global financial flows towards Asia has increased, foreign investors are not dominating or taking over Asian markets as investor access/power is constrained by the developmental logics that inform this opening process. Given the institutional differences within financial opening processes of European and East Asian finance, a growing portion of the contemporary global financial system functions differently from just 15 years ago as global investors must adapt to the developmental characteristics of these markets and play by their rules when allocating investments.

On the other hand, focusing on the growing global footprint of East Asian investment, we can see the persistence of developmentalism in the internationalization of East Asian finance across three levels: (1) through the growth of publicly directed investment flows that deviate from neoliberal norms, (2) through the active role of public authorities in facilitating/managing outward private investment, and (3) by analyzing moments of accommodation/contestation of East Asian developmentalism.

Taken together, we show how East Asia introduces new dynamics into a previously mostly neoliberal global system. More than passively facilitating investment, these public authorities play an active role in directing (strategic investments) and safeguarding (forex operations) investment flows while contesting (currency intervention) and reconfiguring (swap lines/repo facility) global macrofinancial arrangements.

These practices challenge the liberal global financial system as evidenced by the increasing politization of foreign-exchange interventions, growing rhetoric about currency manipulations, or the accommodation of developmental Asian investment through Western central banks. While current academic and policy debates mostly focus on China, we have illustrated that these should rather be understood as characteristic of the growing contestation of neoliberal finance by East Asian financial internationalization.

Overall, we observe that instead of converging with prevailing global norms, Asian finance remains substantially informed by developmental logics despite its increasing financialization and globalization. This makes the composition of the global financial system more heterogeneous, marking a tectonic shift that challenges the neoliberal transatlantic consensus that defined the pre-crisis global financial system.

Our study points towards an important blind spot in contemporary analyses of global finance. Both research that focuses on public money flows driven by reserve-accumulating Asian economies as well as macrofinancial analyses of private international finance need to expand their analytical focus to take into consideration the newly emerging Asian public-private institutional arrangements that entangle public authorities with the investment strategies of financial actors and challenge neoliberal norms of market organization.

In sum, we identify commonalities and differences, both between Asian countries as well as between outward investment and internal markets:

First, as global investors venture into East Asian financial markets, their investment activities are often monitored, regulated and restricted, and they must largely adopt to non-liberal rules of market organization.

Second, while the internationalization of Asian investments is informed by both developmental and de-risking logics, East Asian public authorities nevertheless play an active role in managing investment flows for developmental purposes, introducing new public-private interactions into what had previously been a passively regulated private global financial system.

Third, we identify variation within East Asia: Japanese markets/investors are more in tune with neoliberal ideas, whereas the financial openings of Korea, Taiwan and especially China are much more aligned with developmental characteristics.

Given the scope of this project, more research and a better understanding of Asia’s growing role within the global financial system is needed. While we focused on East Asia, future research should include other Asian financial systems: India and ASEAN economies are among the world’s fastest growing and increasingly internationalizing financial systems with likely developmental characteristics. Growing Islamic finance sectors in Malaysia and Dubai equally challenge liberal norms of market organization. Asian financial centers such as Singapore, Hong Kong and Shanghai are rapidly gaining in significance. And Russia’s financial markets – especially in the wake of Western sanctions after the Ukraine invasion and growing Sino-Russian financial collaboration – also warrant closer scrutiny.

Furthermore, we see moments of contestation as powerful Western financial actors often consider developmentalism as violating the neoliberal rulebook of how global finance should function. Index provider MSCI, for instance, threatened to downgrade China, India and Korea for not properly opening their markets. In the same vein, the US Treasury recently placed several Asian countries on its currency manipulation watch list, and the ongoing US-China trade war equally stems from a clash of neoliberal and developmental logics. How do Asian actors mediate pressures to adopt neoliberal rules? Are these pressures effective or are we instead witnessing the emergence of an Asian financial sphere of influence that is largely informed by developmental logics?

Asia’s growing importance in global finance raises important conceptual considerations for academic research: Are contemporary theories of the (infra)structural power of finance sufficient to analyze non-Western financial systems? Can East Asian developmentalism help us to better understand the recent emergence of more non-liberal practices (e.g., investment screening/bans) in the West within the context of growing geopolitical tensions? Given the backdrop of an increasing geopolitical global finance, more scholarly dialogue between political economy and security studies might be warranted, especially in the context of a financial system where non-Western actors are seemingly gaining power.

Finally, what are the implications for conceptualizations of financial globalization, financialization or neoliberalization in ongoing debates about convergence or path dependency of national capitalisms in the face of a more heterogeneous, potentially more developmental global financial system? With financial activity within the global economy gradually shifting towards the East, more research is needed to explore this new world in which global financial transactions increasingly take place.

This article is adapted from the authors’ paper “East Asia and the politics of global finance: a developmental challenge to the neoliberal consensus?”, which was published on March 15, 2023, in the Review of International Political Economy.

Further reading:

Johannes Petry

Institute for Political Science, Goethe University Frankfurt, and the Centre for the Study of Globalisation and Regionalisation, University of Warwick

Fabian Pape

Department of International Relations, London School of Economics and Political Science

Asia Global Institute

The University of Hong Kong

Room 326-348, Main Building

Pokfulam, Hong Kong

asiaglobalonline@hku.hk

+852 3917 1297

+852 3917 1277

©2026 AsiaGlobal Online Journal

All rights reserved. Terms of Use - Privacy Policy.

Opinions expressed in pieces published by AsiaGlobal Online reflect those of the authors and do not necessarily represent the views of AsiaGlobal Online or the Asia Global Institute.

The publication of AsiaGlobal Voices summaries does not indicate any endorsement by the Asia Global Institute or AsiaGlobal Online of the opinions expressed in them.

Check out here for more research and analysis from Asian perspectives.