In a new book, global finance expert James A Fok identifies the sources of the severe and still growing financial imbalances between the US and China and the geopolitical and geo-economic tensions they have caused. This is, as Fok calls it, a Financial Cold War, which he argues has been underway for decades.

Credit: DesignRage / Shutterstock.com

Recent years have seen a steady escalation in China-US tensions, with many now claiming that the two countries are in a new Cold War. Analogies with the 20th-century conflict between the United States and the Soviet Union, however, are misplaced. At the outset of the Cold War, there was no meaningful trade or investment between the US and the USSR. With virtually no economic relationship to begin with, there was little to lose from strategic disengagement. Today, globalization has interwoven and integrated economies and supply chains around the world to an extent that would make a decoupling between China and the US not only economically damaging, but also quite likely to lead to a cascading set of international conflicts.

How did we find ourselves in this precarious position? And how can current tensions be de-escalated?

Of course, there are many dimensions to Great Power relations. Nevertheless, financial factors have played a significant part in the creation and escalation of conflict between Beijing and Washington. Unfortunately, the financial causes of frictions are not well understood. This is reflected in the focus of the administration of Donald Trump on solving the bilateral trade deficit. In fact, trade accounts for a mere 10 percent of cross-border capital flows; financial flows make up 90 percent. Therefore, to truly understand the imbalances in the Sino-US financial relationship, it is to the capital markets that we must turn.

To a large degree, the conflict we are witnessing today has been driven by a long-standing Financial Cold War, which has been underway for decades. This is the invisible conflict, embedded in national financial policies and the structure of the international financial system, over the distribution of income and wealth. Over the course of history, extreme inequality in the allocation of resources has tended to lead to conflict. Over two millennia ago, the philosopher Mencius had observed the link between the apportionment of farmland and social stability and, in pre-industrial times, rises and falls in Chinese dynasties tracked fluctuations in the ratio of arable land per capita. More recently, the Great Depression contributed to the rise of Nazism and the outbreak of World War II. Contemporary political leaders ignore the lessons of history at their peril.

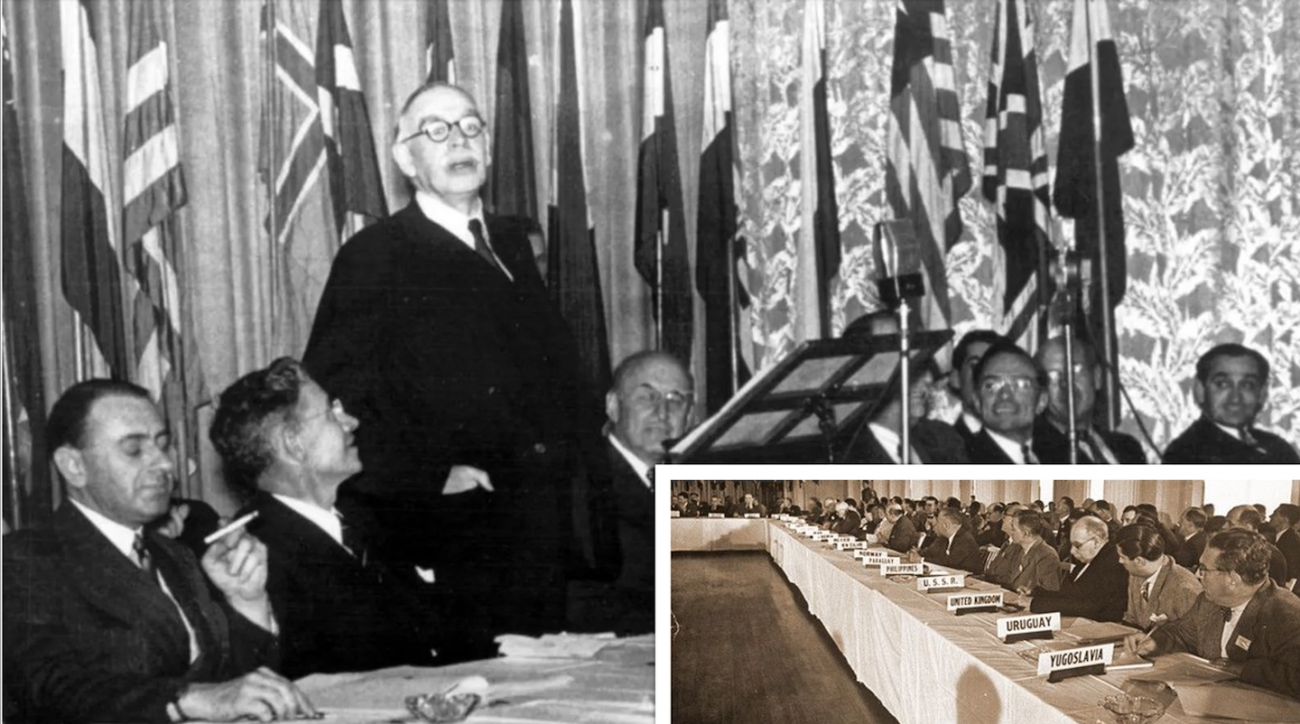

The opening shot of this Financial Cold War was the Bretton Woods Agreement of 1944, which lodged the US dollar at the center of the global monetary system. Financial systems, like all ecosystems, thrive on equilibrium. The dollar’s centrality in the international financial order spawned an imbalance that has since grown and multiplied. The war has played out over two key battlefronts.

The first has been the division of resources between countries. The dollar-centric global financial system has created international demand for dollars that has provided the US with abundant low-cost capital. Other countries, notably emerging markets that have found themselves at the mercy of volatile hot money flows, have borne a high cost for this. However, to keep the world supplied with sufficient dollar liquidity to support growing international trade and investment, the US has been required to run continual balance-of-payments deficits. The lack of any structural mechanism for revaluing the currencies of countries with persistent large surpluses has transferred productive capacity to other centers and contributed to growing American indebtedness. This has had an impact on US fiscal and monetary policies and, given the dollar’s central role in global financial markets, generated financial instability around the world.

The second battlefront has been over the distribution of wealth within countries. The billionaire Warren Buffett candidly told a CNN reporter in 2011 that “there’s been class warfare going on for the last 20 years, and my class has won”. He was right. Structural overvaluation of the dollar has disproportionately benefited the wealthy, as corporate profits have been boosted by outsourcing to lower-cost countries, while US workers have paid the price. This is not just a matter of monetary policy, however. Since the 1980s, extreme ideological leanings towards “free market” policies have led to more regressive tax policies, less rigorous antitrust enforcement, and soaring executive compensation.

China’s rapid growth over the past four decades and the consequent improvement in the country’s living standards have insulated it to an extent from this second battlefront. As the events of 1989 bore witness, however, market-oriented reforms generated considerable social tensions. Further, the government’s suppression of domestic consumption to drive infrastructure and other investment, while successful in achieving rapid economic growth in earlier years, is now contributing to soaring inequality and exacerbating structural imbalances. In the face of the country’s rapidly aging demographics, continued dependence on its top-down investment-led economic model runs the risk of growing resource misallocation. Attempts to export its excess industrial capacity through the Belt and Road Initiative (BRI) have created international frictions. Meanwhile, the stunted development of China’s domestic financial markets means that the rising social welfare burden will weigh considerably on national finances.

In the face of growing domestic social tensions, political elites in both countries have resorted to populist nationalism. The result has been escalating Sino-US tensions, with the Financial Cold War heating up in the form of a widening geo-economic clash.

Since the Trump Administration launched its trade war with China in January 2018, the scope of the conflict has been extended far beyond trade tariffs. Sanctions have been applied against Chinese technology companies. US allies have been pressured to remove Chinese manufactured components from their telecommunications networks. Further, Chinese companies from sensitive sectors have been denied access to US capital markets. Officials from both countries have hurled incendiary accusations at each other and engaged in an unseemly war of words over the origins of the Covid-19 pandemic and interference in Hong Kong affairs. As the geo-economic clash between the China and the US unfolds, there is a substantial risk that this will spill over into broader conflicts that could result in disaster for both nations and the rest of the world.

In practice, the most potent weapon that the US has in its geo-economic arsenal is its influence over the dollar and dollar payment systems. In recent years, Washington has wielded this forcefully in the pursuit of unilateralist agendas. Continued abuses of this geo-economic endowment, however, could precipitate its own downfall, as even traditional US allies have been looking to reduce their dependence on the dollar-based system. One example was the decision by Britain, France and Germany to create the Instrument in Support of Trade Exchanges (INSTEX) in the wake of Trump’s withdrawal from the UN-backed Iran nuclear deal.

In the face of rising threats of US sanctions, China has also sought to reduce its vulnerability. This has included setting up the Cross-Border Interbank Payment System (CIPS) as an alternative to the established SWIFT bank-messaging network and developing its central bank digital currency. These steps are intended to support a more international role for the renminbi in trade settlements. The major factor preventing the renminbi from becoming more widely accepted in global trade, however, is the difficulty international investors have in investing yuan-denominated proceeds. Programs that have channeled investment through Hong Kong have helped increase international appetite for Chinese domestic securities but, to truly internationalize the renminbi, it will be necessary to expand significantly the pool of renminbi securities offshore and to loosen the government’s tight control over China’s financial system.

There are good reasons for Chinese policymakers to proceed cautiously, though. They are acutely aware of the enormous costs the US has borne due to the dollar’s global role and are wary of the volatility associated with liberalizing cross-border capital flows. Unlike the US, China also has limited ability to enforce its anti-tax evasion laws overseas. Further, given America’s control over major international custody and depository infrastructures, greater outbound securities investments by Chinese corporations and individuals would expose China to further risks of the type of financial sanctions that have been applied against Russia. This standoff is ironic, as both countries would benefit from greater outbound investment by China’s savers and a more international renminbi.

Worryingly, the cracks in the dollar-based global monetary system were starkly highlighted by the extraordinary drying up of liquidity in the US Treasury market in March 2020, amid global panic over the economic impact of Covid-19. Financial collapse was averted when the Federal Reserve stepped in to buy up US government and other securities. Since then, US government spending on pandemic relief and stimulus measures has soared; however, this is no longer being funded by international demand for US sovereign debt, but by an unprecedented expansion in the Federal Reserve’s balance sheet.

Concerns over currency debasement have contributed to a surge in interest in cryptocurrencies. Whether such novel challengers to the dollar will pose a serious long-term threat remains to be seen. Growing financial imbalances, however, risk exacerbating both domestic social tensions and international conflicts, and soaring public debt threatens today’s younger generation with unsustainable burdens that will imperil future prosperity and stability.

Nevertheless, markets operate within institutional frameworks and are subject to the incentives that they create. It is, therefore, incumbent on responsible leaders to work together, seek truth from the facts, and design policies that address the sources of current Sino-US tensions. The sheer scale of the financial imbalances that have built up means that they cannot be quickly unwound.

Both Chinese and US leaders appear to have recognized the need to address rising domestic inequality. While some may criticize the lack of due process, Chinese leader Xi jinping’s “common prosperity” initiative is an attempt to tackle the causes of income disparity and to redistribute China’s wealth. Given the greater constraints of American constitutional democracy, the Biden administration has faced tougher opposition to fiscal redistribution. Further, its open markets, coupled with the highly mobile nature of international capital, mean that it must necessarily seek international support. US Treasury Secretary Janet Yellen’s push for a global minimum rate of corporate tax is a good first step but, as University of British Columbia (UBC) professor Wei Cui makes clear in a recent AsiaGlobal Online article, much still needs to be done to give teeth to these measures.

Addressing the problems created by the dollar’s global role will be more challenging. While the pound sterling’s transition from its role as the dominant global reserve currency in the decades after World War II provides a precedent, the scale of imbalances in the dollar system today, as well as the complex system of dollar-based derivatives and collateral that has developed, makes reducing international dependence on the dollar far more complex. And what would replace it?

Former People’s Bank of China (PBOC) governor Zhou Xiaochuan has suggested elevating the role of the Special Drawing Rights (SDRs) of the International Monetary Fund (IMF). To replace the dollar as a global utility, however, a large pool of SDR-denominated investments would need to be built up, along with the hedging and other financial instruments needed to support international trade and investment. There is also an important question of governance. As seen during the euro crisis, international disagreements can paralyze decision-making at multinational institutions, causing delays that can have severe economic consequences.

A rebalancing of the Sino-US financial relationship would help reduce tensions and bring substantial benefits to both countries. Any progress in this regard will depend on rebuilding trust. The current generation of leaders has inherited many serious challenges and, given current tensions, the compromise and cooperation needed to fix our global financial system may not come easily. For the sake of our future peace, stability and prosperity, however, this is a task that can no longer be put off.

Further reading:

Asia Global Institute

The University of Hong Kong

Room 326-348, Main Building

Pokfulam, Hong Kong

asiaglobalonline@hku.hk

+852 3917 1297

+852 3917 1277

©2025 AsiaGlobal Online Journal

All rights reserved. Terms of Use - Privacy Policy.

Opinions expressed in pieces published by AsiaGlobal Online reflect those of the authors and do not necessarily represent the views of AsiaGlobal Online or the Asia Global Institute.

The publication of AsiaGlobal Voices summaries does not indicate any endorsement by the Asia Global Institute or AsiaGlobal Online of the opinions expressed in them.

Check out here for more research and analysis from Asian perspectives.