The documentary “The China Hustle” exposes fraudulent transnational listings that are costing millions of investors billions of dollars. How can stock markets around the world combat this major threat to the global economy? The answer may lie in extraterritoriality.

Filmmaker Jed Rothstein’s documentary The China Hustle tracks a number of fraudulent Chinese companies that have listed on US stock markets. Despite the illegality of these companies’ activities, American law enforcement could not pursue those behind them, because they live and work in China. Millions of investors have lost billions of dollars because national borders protect fraudsters. Is all of this simply an unavoidable feature of the global economy?

Our research shows that countries looking to prevent that kind of transnational fraud can utilize a legal principle known as extraterritoriality. Extraterritorial laws allow police and prosecutors to work across borders. These kinds of laws would increase stock market valuations of Chinese companies in Hong Kong by about 7%.

What is Extraterritorial Corporate Governance?

Extraterritoriality involves applying one country’s laws in foreign countries. This concept is not new, even in the context of corporate governance regulations. The most well-known extraterritorial laws relate to corruption and competition. American prosecutors have the power to convict people for engaging in what the US defines as bribery or collusion in another country, even if these individuals commit the offences in countries where such activities are legal.

In the case of corporate governance, two US laws give American prosecutors limited extraterritorial powers: the Sarbanes-Oxley Act and the Dodd-Frank Act. One may assume that such legislation would scare off foreign companies from listing in the US. Yet, the data show the opposite.

Over two decades of economic theory and data analysis show that firms prefer tougher securities enforcement.

The data show that corporate governance rules, which put into place potential punishments for corporate malfeasance committed across borders, increase stock market valuations. The Sarbanes-Oxley’s tough and extraterritorial corporate governance rules generated higher “excess returns” (or returns above the market average) on foreign firms’ valuations.

Over two decades of economic theory and data analysis show that firms prefer tougher securities enforcement, because these rules reassure investors about the quality of the companies they invest in. The bump-up comes from investors’ trust in these companies’ better corporate governance rules—and the increased likelihood of these rules’ enforcement.

Why Would Stock Markets Want Extraterritorial Enforcement?

Many countries may wish to bind their stock markets to such cross-border laws. The creation of the European common banking and securities regulation space has already helped bind European countries’ stock markets to cross-border enforcement. However, without law enforcement agencies like the FBI, which has international offices, European police and prosecutors have fewer chances to take advantage of such enforcement possibilities.

Going back to Asia, Hong Kong is a jurisdiction that would naturally benefit from such extraterritorial enforcement with China. In our study, we show that binding mainland companies to Hong Kong’s better corporate governance rules would increase these companies’ market valuations by about 7%. This, however, would only be the case for companies actually listed on the Hong Kong Stock Exchange. Also, the study merely reveals the effect of better rules, not that of better enforcement.

Binding mainland companies to Hong Kong’s better corporate governance rules would increase these companies’ market valuations by about 7%.

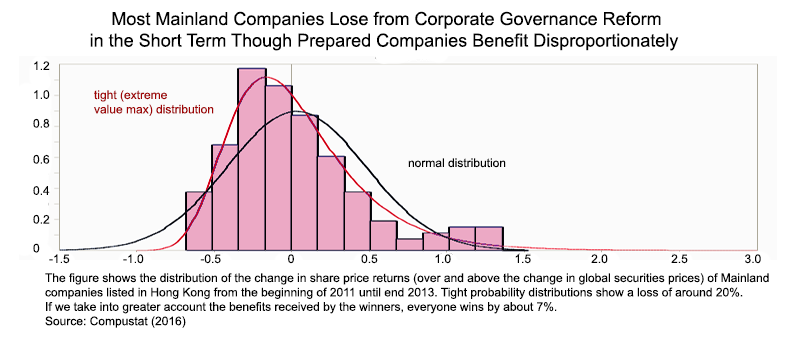

Better rules and enforcement would hurt as well as help some companies. The figure below shows a roughly 7% increase in market valuations of Hong Kong-listed mainland companies after they adopt Hong Kong’s better corporate governance rules. This overall improvement, though, conceals a large number of companies harmed by better corporate governance rules and enforcement. The left tail of this statistical distribution shows the companies with decreased market value. These include companies that rely on bad practices, as they would lose investor confidence and perhaps even face criminal penalties under better-defined rules.

The China Hustle shows us that the US Department of Justice and Securities and Exchange Commission do not always enforce their extraterritorial corporate governance rules. As we argue in our paper, a jurisdiction like Hong Kong, with the ability and incentives to enforce these rules, might win listings away from the US stock exchanges.

Hong Kong’s lawmakers must first put such extraterritorial provisions into their securities and corporate governance laws. They must have procedures in place for conducting random audits/inspections and for collecting evidence abroad. They must get the permission of these companies to undertake these inspections, and must have standing in foreign courts to bring civil and/or criminal cases.

A jurisdiction like Hong Kong, with the ability and incentives to enforce these rules, might win listings away from the US stock exchanges.

Based on our analysis for Hong Kong, what can other jurisdictions looking to make their own stock markets more competitive do? They must think about inserting extraterritorial provisions into their own securities—and even criminal—laws. They must show that their stock market authorities can organize inspections abroad on foreign domiciled companies listed in their jurisdiction. They must also have procedures in place for dealing with investor complaints about their foreign companies; as well as procedures for dealing with other countries’ authorities.

When corporate governance law allows for such better policing, the China hustle will end.

Further Reading

Michael, Bryane and Goo, Say Hak, "The Role of Hong Kong's Financial Regulations in Improving Corporate Governance Standards in China: Lessons from the Panama Papers for Hong Kong" (November 1, 2016). University of Hong Kong Faculty of Law Research Paper No. 2016/048.

Asia Global Institute

The University of Hong Kong

Room 326-348, Main Building

Pokfulam, Hong Kong

asiaglobalonline@hku.hk

+852 3917 1297

+852 3917 1277

©2026 AsiaGlobal Online Journal

All rights reserved. Terms of Use - Privacy Policy.

Opinions expressed in pieces published by AsiaGlobal Online reflect those of the authors and do not necessarily represent the views of AsiaGlobal Online or the Asia Global Institute.

The publication of AsiaGlobal Voices summaries does not indicate any endorsement by the Asia Global Institute or AsiaGlobal Online of the opinions expressed in them.

Check out here for more research and analysis from Asian perspectives.