The adoption and use of central bank digital currencies in the Asia Pacific depend on their value-added for businesses and end-users and the support from banks and payment service providers, write Sally Chen, Tirupam Goel and Han Qiu of the Bank for International Settlements.

Credit: thodonal88 / Shutterstock.com

With the objectives for issuing central bank digital currencies (CBDCs) becoming increasingly clear and a growing number of central banks running pilot retail CBDC programs, many observers are assessing the benefits and cost of CBDCs for the broader population. For many central banks, CBDCs are a necessary pursuit in an increasingly digitalized world. Encouraging CBDC adoption, however, is challenging, especially in the presence of effective and efficient payments alternatives (eg, Faster Payment System, or FPS; cash).

Indeed, the success of CBDCs depends on having end-users, businesses, banks and payment service providers (PSPs) on board. The envisioned benefits of CBDCs would be of little use and their viability at risk if adoption is too low. This issue is particularly relevant for many Asia-Pacific economies where the payment infrastructure is generally efficient and resilient and where digital payments are already widely used.

To shed light on this issue, we first review the experience of a previous central bank initiative at mobile payments innovation. We then consider how Asia-Pacific economies compare along a number of payment dimensions to draw lessons for CBDC adoption.

Past experiences with central bank payment innovations can offer valuable lessons on CBDC adoption. Specifically, we look at the experience of Ecuador’s mobile payment initiative, Dinero Electrónico (DE), a mobile payment system developed by Banco Central del Ecuador (BCE), Ecuador’s central bank, in 2014.

The DE experience offers two lessons: that user preference is foundational in CBDC design and that the support of incumbent banks is critical for success. DE’s take-up among end users was immediate and sizable as it was easy to sign up – no application or initial deposits were needed – and easy to use – internet access was not required while transfers between accounts were in real time, seamless and low cost. But support from existing payment service providers was lacking. Without it, DE could not reach the scale it needed for permanence. (The flipside of low adoption is broad-based adoption. In the case of CBDC, this can disintermediate private banks and thus threaten financial stability, which is a concern for central banks. As such, central banks envision a level of adoption that threatens neither bank intermediation nor the viability of the CBDC initiative.)

Ecuador’s experience with DE suggests that satisfying the payment preferences of end users and engaging with intermediaries (such as banks and PSPs) – dimensions beyond technology – are crucial CBDC design considerations. We consider these dimensions for the major economies in Asia Pacific below.

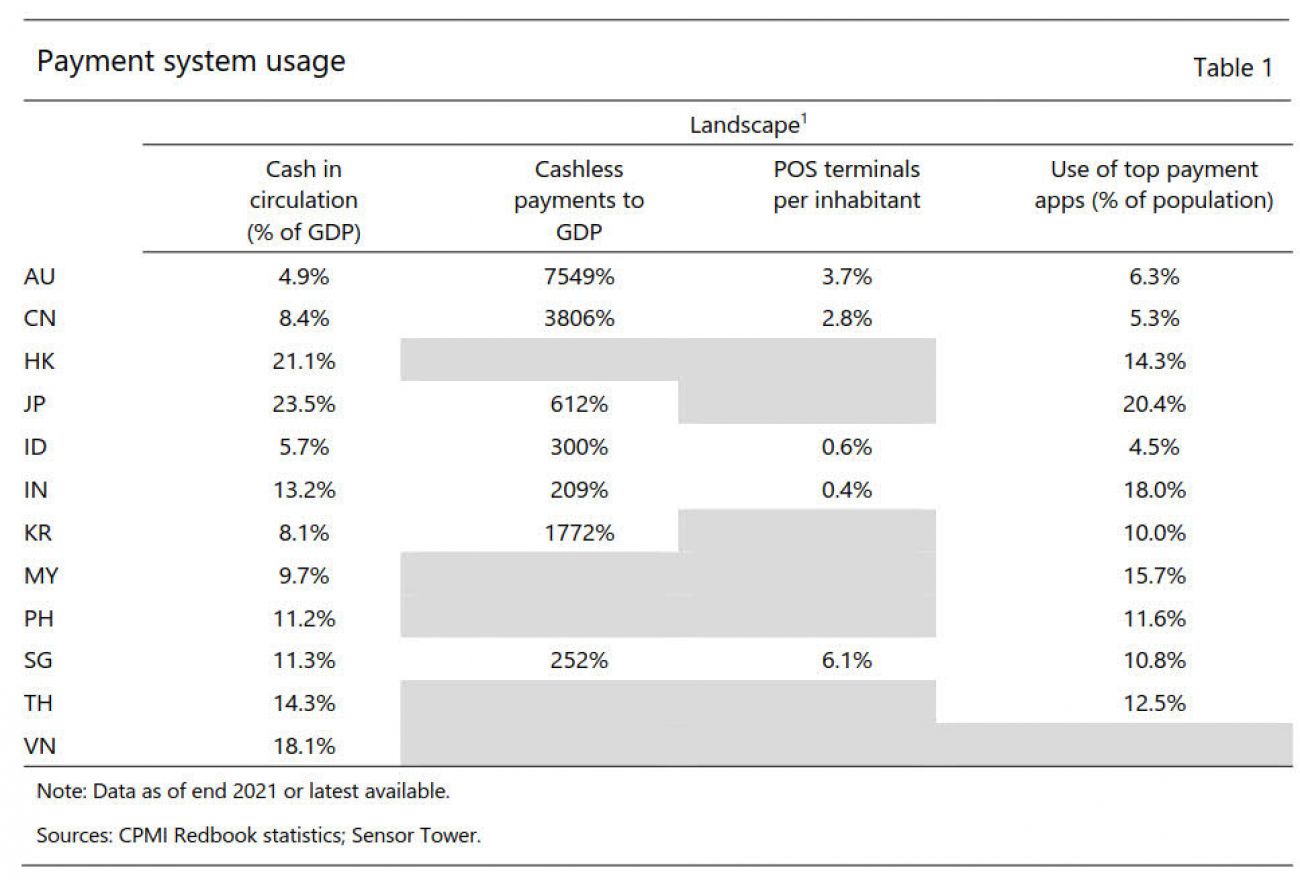

A necessary condition for CBDC adoption in payments is to satisfy the target audience’s payment preferences. To understand these preferences, we review the usage pattern of payment systems in the region (Table 1). We uncover a key characteristic that is unique to Asia Pacific: It is a region with still strong cash use alongside advanced digital payments.

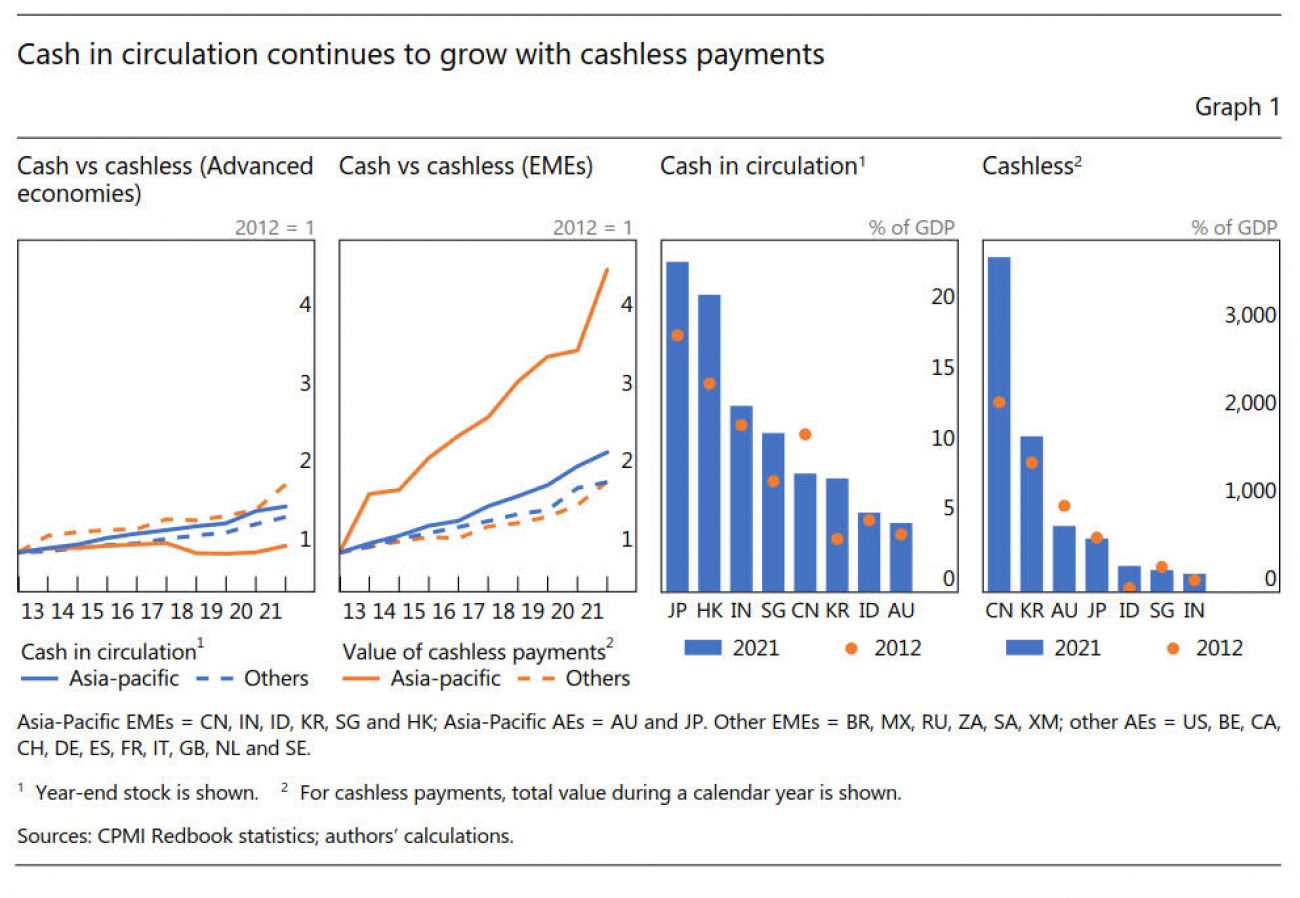

Cash maintains an enduring appeal in many economies Cash in circulation has grown alongside cashless payments (Graph 1, first and second panel). It is generally hard to obtain data on the total value of cash-based payments. Cash in circulation can serve as a proxy for cash-based payments assuming that the multiplier (ie, the velocity of physical cash) stays constant over time. Hong Kong, Japan and Singapore, for example, saw sizable increases in cash in circulation over the last decade (third and fourth panel). This increase in many economies, including those with advanced payment systems, suggests that infrastructure and technology are but one of many factors that shape payment preferences. A pilot survey conducted by the Reserve Bank of India (RBI) on retail payment habits of individuals showed that cash remains the preferred mode of payment, particularly for small-value transactions, despite the existence of an efficient payments system and recent innovations.

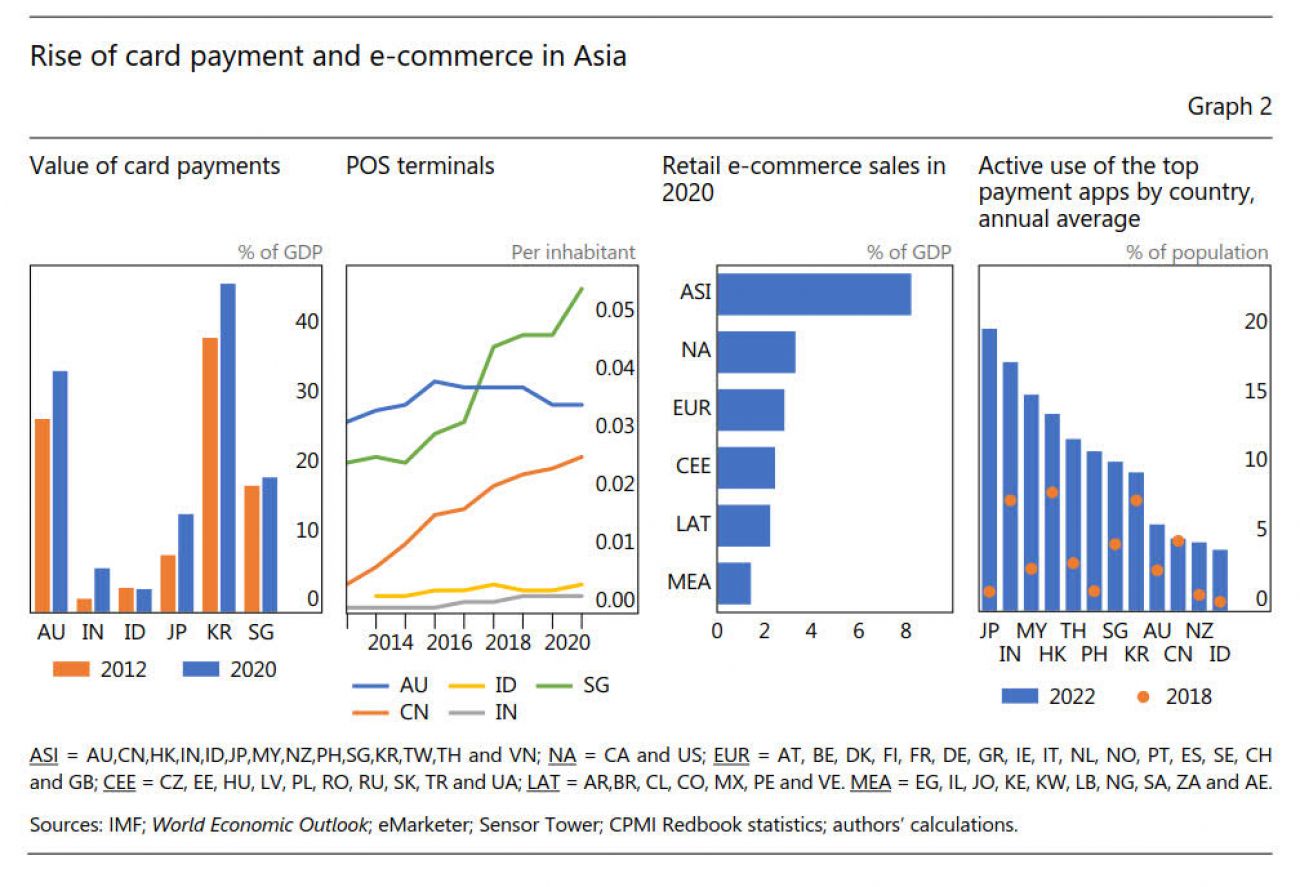

Digital and payment infrastructures are advanced In Asia Pacific, cashless transactions have risen, with widespread e-commerce and fintech (Graph 2). Indeed, the share of the population in advanced economies in Asia Pacific using the internet reached almost 90 percent before the Covid-19 pandemic, while e-commerce expanded rapidly. E-commerce grew by nearly 60 percent on an annual basis in 2020 in Indonesia and by roughly 40 percent for Vietnam over the same period. In the Philippines, e-money accounts are now the most widely owned type of account, with users growing more than fourfold in just two years. In total, Asia Pacific now has the largest share of e-commerce in the world. This growth in e-commerce has helped create strong demand for digital payment solutions (Graph 2, third and fourth panel).

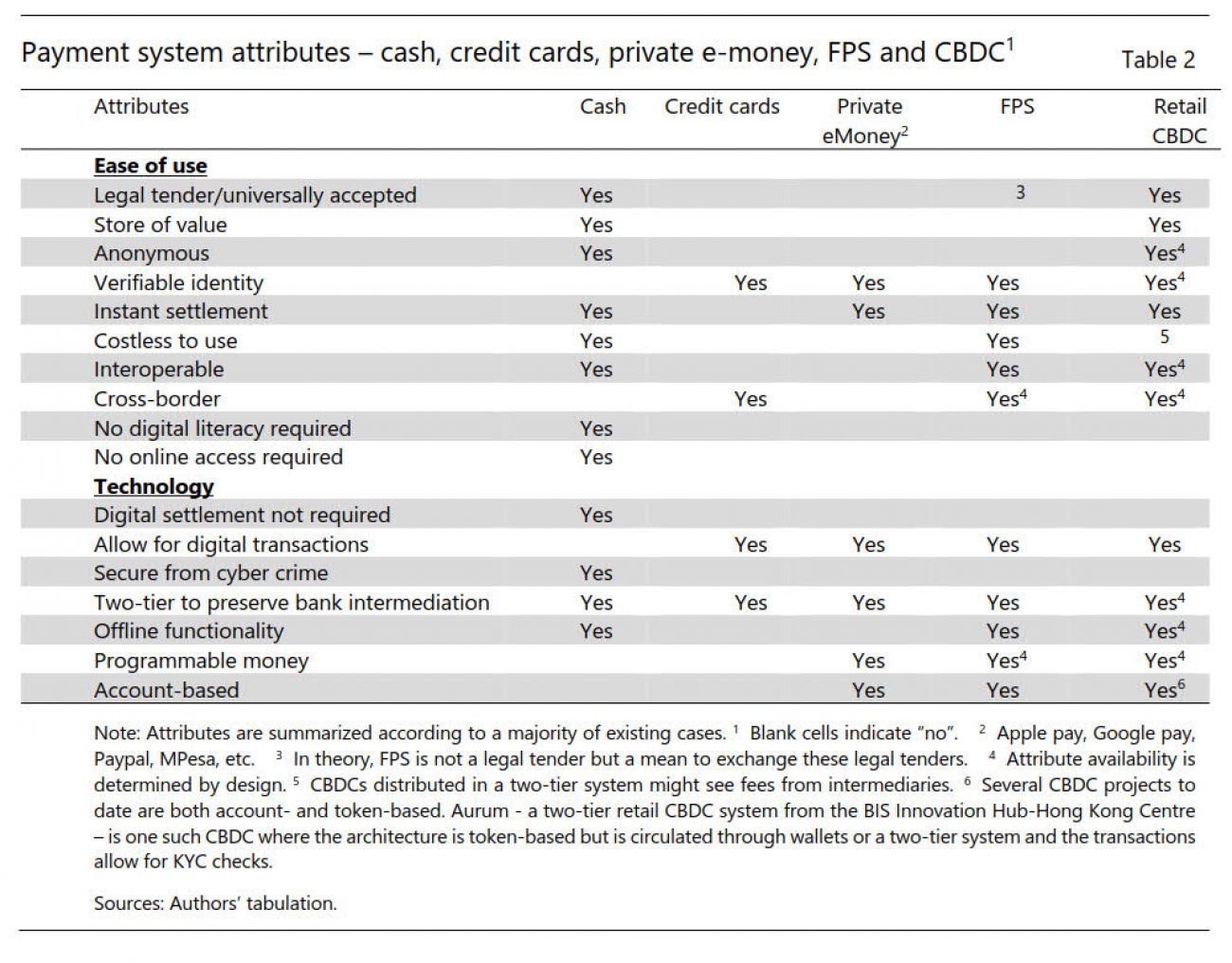

Where do CBDCs stand relative to other payment methods in terms of benefits and costs? Given the growing prevalence of digital means of payments in Asia Pacific and an enduring preference for cash, do CBDCs offer added value compared to other instruments? Needless to say, what CBDCs can offer to each economy depends on their design as well as economy-specific payment system attributes. Nonetheless, comparing the attributes of CBDCs with those of existing payment options suggests some common themes for design consideration (Table 2):

The first is that cash ranks high on usability. Cash offers anonymity, a feature none other can fully replicate at the current juncture. Second, the room for flexible use cases is limited with cash, as it lacks many of the advances associated with financial technology. Third, technological innovations evolve as a continuum. Programmability, which has been promoted with distributed ledger technology (DLT)-based platforms, is now increasingly available to others. Indeed, some second-generation systems such as the Unified Payment Interface (UPI) in India admit certain types of programmability.

For Asia-Pacific, this overview of current payment system usage patterns and CBDC attributes suggests two key considerations that public authorities must consider for a viable level of CBDC adoption:

First is a design that is user-centric and future-proof. Advanced digital and payment infrastructure, combined with the widespread use of e-commerce and fintech in the region make it imperative that CBDCs meet the needs of an increasingly digitalized society. CBDC design, therefore, must allow for easy adaptation to technological changes. At the same time, the enduring appeal of cash, even in Asia-Pacific economies with a high level of digitalization, suggests that CBDCs need to address concerns for transactional privacy and incorporate physical cash’s usability features more broadly (eg, offline access).

Current CBDC experiments and experiences suggest that there can be fruitful design combinations. For example, Project Rosalind of the BIS Innovation Hub London Centre is exploring voice-authenticated payments and cognitive accessibility for inclusion. Project Tourbillion from the BIS Innovation Hub Swiss Centre makes use of “blind signatures” that allow central banks to issue retail CBDCs without knowing the identity of the holder. The project also uses “mixed networks” that prevent the traceability of communications between customers, banks and central banks.

Second, CBDC design must internalize bank-specific considerations that are different from end-user considerations. There are competition concerns – eg, potential disintermediation or crowding out of banks and PSPs by CBDCs. There are also revenue concerns – eg, payment service fee income for banks could come under pressure from CBDC issuance. Finally, there are incentive issues – ie, intermediaries may not find it profitable enough to participate in the CBDC architecture.

The introduction of Pix – Brazil’s fast payment system – suggests that banks and PSPs need not suffer if digital payments, including CBDCs, are suitably designed. Pix is positioned as an alternative to existing payment instruments that helps reduce transaction costs. While banking fee income, including revenues from domestic TED payments (Transferência Eletrônica Disponível – is an electronic transfer method that allows for real-time money transfers between bank accounts with no limit on the transaction amount), had initially stagnated after its introduction, banks’ service fee income, including Pix fees and non-payment revenues have grown since November 2020 as Pix usage increased swiftly.

Brazil’s experience suggests that if CBDCs come with greater interoperability, ie, allows for multiple payment systems to be connected, a corresponding increase in payment system usage and transaction volume could boost banks’ service fee income. Put differently, features that enhance usage, including programmability and cross-border transactions could bring greater opportunities to banks to expand their user base.

The viability of CBDC initiatives depends on adoption. CBDCs must meet users’ preferences – eg, the need for privacy and usability – and address commercial banks’ concerns around disintermediation. At the same time, new functionalities – eg, offline access – could enhance CBDCs’ appeal, while interoperability could broaden payment channels, both of which help boost user adoption.

Experience suggests that securing the success of CBDCs requires a long and broad horizon. For economies that already have efficient and sophisticated payment systems, the benefits of CBDCs to end users might not be immediately apparent. Here, it is useful to remember that technological innovations can shape user behavior and preference, as seen in the rapid expansion of digital payments and e-commerce in Asia. The broad-based adoption of e-commerce, for example, was driven in part by infrastructure developments. Central banks thus need to take a long view. Indeed, for many, CBDCs are part of the ongoing digital revolution – a necessary endeavor that allows central banks to continue to provide an anchor for monetary stability in an increasingly digitalized world.

The views expressed in this article are those of the authors and do not necessarily represent the views of the Bank for International Settlements (BIS). The authors thank Jimmy Shek for invaluable assistance and Stijn Claessens, Jon Frost, Bénédicte Nolens, Ilhyock Shim, Siddharth Tiwari and Tao Zhang for thoughtful discussions and comments.

Sally Chen

Bank for International Settlements (BIS)

Tirupam Goel

Bank for International Settlements (BIS)

Han Qiu

Bank for International Settlements (BIS)

Asia Global Institute

The University of Hong Kong

Room 326-348, Main Building

Pokfulam, Hong Kong

asiaglobalonline@hku.hk

+852 3917 1297

+852 3917 1277

©2026 AsiaGlobal Online Journal

All rights reserved. Terms of Use - Privacy Policy.

Opinions expressed in pieces published by AsiaGlobal Online reflect those of the authors and do not necessarily represent the views of AsiaGlobal Online or the Asia Global Institute.

The publication of AsiaGlobal Voices summaries does not indicate any endorsement by the Asia Global Institute or AsiaGlobal Online of the opinions expressed in them.

Check out here for more research and analysis from Asian perspectives.